The current state of the bond market

Do low prices present a buying opportunity?

Bond prices have fallen so low that many are saying the current situation presents itself as a buying opportunity.

But there has been plenty of volatility on the bond markets in recent months, and questions arise over what kind of reasons would prompt one to invest in bonds.

Similarly, which type of bond should one invest in, and what kind of place do they take in an investor's portfolio? Are we about to enter a new phase of dynamics in the bond market as central banks' bond buying programmes come to an end?

This report hopes to answer some of these questions, and is worth an indicative 30 minutes' CPD.

Advisers are starting to find bonds more interesting as an investment, despite the sharp price falls this year, according to the latest FTAdviser Despatches poll.

The online poll ran from November 1 to November 21, and asked the question: “Are bonds now a buy?”

By a majority of 67 per cent to 33 per cent, respondents agreed that fixed income assets are now an attractive proposition.

Most bonds have suffered sharp price falls this year as investors feared that the consequence of higher inflation would be a destruction of the spending power of the income from the bond, and that higher interest rates would lead to the price of bonds falling.

But bonds, particularly government bonds, are historically viewed as being lower risk than equities, and so it may be that bonds become more relevant in portfolio construction terms in the coming year as recession fears start to trump inflation concerns.

david.thorpe@ft.com

Things have gotten so bad, says Nicolas Trindade, bond fund manager at Axa Investment Management, that there is now an opportunity.

By this he means bond prices have fallen so far this year, and consequently yields have risen so much, that there are a lot of opportunities in the asset class.

On the reasons for the sell-off this year, Isaac Stell, fund research manager at Parmenion, says: “The unprecedented losses experienced in 2022 are linked to the spike in yields on the back of future interest rate expectations.

“Bonds that have a longer maturity profile experience larger losses during these times due to the higher degree of sensitivity to the interest rate movements.

“This can explain why the typically more defensive assets such as gilts have fallen so far this year. Index-linked gilts have experienced even larger falls despite the inherent inflation linkage as they are also suffering from a negative ‘real yield’.

“Given that interest rates have been at historical lows since [the global financial crisis] and lower still during the pandemic the likelihood of capital gains diminished to almost nothing from a theoretical standpoint. Any movement up in rates from the lows of 0.1 per cent were always likely to reverberate within the bond market.”

Phil Milburn, co-head of fixed income at Liontrust, elaborates on this by saying: “From 2011 onwards we had to sit in front of clients and tell them bonds were expensive and yields were very low.

“That was the result of central bank bond buying programmes, which effectively manipulated markets for a decade. But now that is changing; I’m not saying markets are completely free of manipulation now, but there are at least opportunities.

“For the past decade it was quite a luxury for bond managers as bond prices just kept going up, but this is the first time since 2011 that government debt is cheap, and I would rather sit in front of clients and talk about that.”

Central concerns

Central bank bond buying programmes, known as quantitative easing, are being reduced and unwound in the coming months, at the same time that many governments are increasing their level of borrowing in order to combat imminent recession.

This creates an imbalance between the supply of bonds on the market and demand for those bonds, which has pushed prices downwards and yields upwards.

And while bond yields have risen markedly this year, they remain negative when inflation is factored in.

The manipulation to which Milburn refers was the bond buying programme, which created an excess of demand for bonds over the supply of bonds, keeping bonds at prices he regarded as unnatural.

Frederic Tache, head of fixed income at St James's Place, says the major driver of volatility in the bond markets this year has been investors moving to shorter-duration assets to protect against inflation, “and this means the bonds of even quality companies have sold off”.

Kelly Prior, a fund manager on the multi-manager team at Columbia Threadneedle, is of the view that prices in areas such as investment grade are at a level that represents “a multi-decade opportunity”, due to the lower valuations.

Milburn says the net effect of this change is that the traditional inverse correlations between bonds and equities are returning, and as this is one of the core reasons many advisers and fund buyers allocate to bonds, it may boost demand for the asset class.

Get shorty

Peter Fitzgerald, multi-asset investor at Aviva Investors, says the current elevated levels of bond volatility are the inevitable consequence of quantitative easing coming to an end: “QE killed bond market volatility but now it is back. I think the question for allocators is whether the long-term investment case for government bonds has changed.

“There has been a view that government bonds are in a portfolio to provide diversification and reduce volatility. But this year the 10-year gilt has lost over 20 per cent (at the time of writing, and I am not comfortable with the idea that a client could lose that much in a year and be told to expect it.)”

His solution is to embrace government bonds with a shorter date to maturity; he says that right now, the income from these bonds is attractive, “and you are not getting paid” to take the extra risk of owning bonds with a longer date to maturity.

Traditionally, investors buy government bonds with a longer date to maturity when they fear recession. The logic is that, in order to combat the recession, central banks will cut interest rates.

If rates are falling, then the opportunity to lock in the higher rates offered by a bond today are more attractive, and the longer the time period one can lock the higher income in for, the better.

But Fitzgerald says it will be different this time because, while tighter monetary policy likely caused the recession, the extremely high rate of inflation means central banks may not be able to cut rates, and so the benefits that typically accrue to investors in long-dated bonds in a recession will not happen.

He says that while he has been increasing his government bond exposure, “it is right at the front end of the curve”, (the shortest possible duration).

Fitzgerald says the traditional market view, that bonds and equities are negatively correlated, only holds true when interest rates are lower than about 5 per cent, as above that level both bonds and equities tend to fall.

Cash for carry

Giles Dauphine, deputy chief investment officer for fixed income at Amundi, says the main reason clients are buying bonds right now is to get access to the higher yield, rather than for the diversification benefits, but he says the traditional diversification benefits are returning.

Of course, the income from a bond is only of use to a client if the borrower actually has the cash to pay.

In the QE era, cash was so plentiful and yields so low that this was seldom a problem, but as those factors reverse, it is likely to become another issue of concern for advisers and their clients.

Michael Matthews, a bond fund manager at Invesco, says fixed income investors right now are worried about both higher inflation and recession, and the challenge is that different parts of the bond market offer protection from only one of those at a time, but he says yields have now risen to a point where “bonds are pulling in money from other asset classes again”.

Matthews' view is the initial sell-off in bonds was the result of the market being aware that governments are increasing the amount of debt they issue, at the same time that central banks are no longer buying; he feels the recent uptick in demand for the assets is the result of yields rising to a level where even sceptical investors are tempted.

Milburn notes that even the investment-grade corporate bond index in the US is yielding around 6 per cent, a number that would imply that a higher than average level of defaults is being priced into markets.

But this is not something Milburn says he is expecting to happen. He says: “Usually a larger default cycle happens when one particular sector is in trouble, and after a period where there has been a boom in that sector, but there is no obvious problem child in it at the moment.”

Tache says default rates in bonds are presently around 1 per cent to 2 per cent, and even if this were to rise to 2 per cent to 3 per cent, “it would still be low relative to history”.

He says defaults are less likely to be about sector level exposure this time and more about the level of debt firms have.

Nevertheless, he says that he feels defaults will rise, but only towards the long-term average. With this in mind he says he is “avoiding the lowest quality and most cyclical parts of the market, particularly in high yield – we won’t go near the CCC segment, there is just too much uncertainty around for me to want to go near there”.

Fahad Kamal, chief investment officer at Kleinwort Hambros, is another who says defaults will pick up, but not to problem levels.

Paul Angell, investment research analyst at Square Mile, says despite yields being much higher they are still negative in real terms, “and so if you want to make a positive return after inflation from a corporate bond, you probably need capital gain as well, and that would likely need to come from interest rates falling”.

Rate of decline

Falling interest rates is something Milburn says could be on the horizon, albeit not until well into 2023.

In addition to a view that recession is coming, he says he feels that inflation in the US has already peaked at the headline level, and that housing inflation will peak and start to decline next year, leading to overall inflation falling, and reducing the pressure on the Federal Reserve to put rates up.

He also says that the long-term path is that factors such as demographic change and debt levels will restore inflation to the very low levels seen prior to the pandemic, creating a situation where bonds would be expected to perform very well.

In contrast, he takes the view that if inflation were to normalise at a level of around 4 per cent, “then I would take the view that bonds are a sell at the current price levels, but I do not think that will happen”.

Kamal has been increasing his exposure to bonds, but only gradually, and remains very sceptical on the asset class.

He says the past decade or so of very low interest rates and inflation is “the anomaly”, and what is happening now is closer to the normal.

John Towner/Unsplash

John Towner/Unsplash

Annie Spratt/Unsplash

Annie Spratt/Unsplash

Regularguy/Unsplash

Regularguy/Unsplash

'Corporate bonds currently offer the best buying opportunity of the decade'

So says Stephen Snowden, Artemis’s head of fixed income at Artemis.

We summarise his thoughts in four key charts.

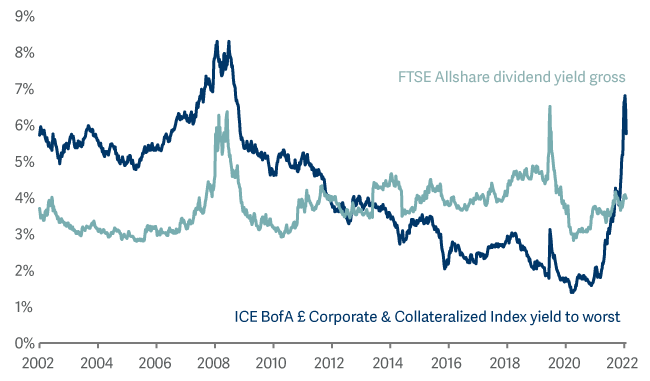

1. Corporate bond yields are at very attractive levels

Corporate bond yields are made up of two components, the underlying gilt yield and the additional spread for the extra credit and liquidity risk.

Over the last few months, 10-year gilt yields have moved to levels not seen for over 10 years.

Meanwhile, credit spreads, while not at levels seen during the global financial crisis, are certainly elevated. Neither gilt yields nor credit spreads are at their peak, but the two combined mean that the overall yield on corporate bonds is around 6 per cent.

When both gilt yields and credit spreads are evaluated, the all-in yield is high

Source: Bloomberg as at October 31 2022

Source: Bloomberg as at October 31 2022

2. Corporate bond yields are now higher than equity dividend yields

The decade or so of quantitative easing suppressed corporate bond yields to the extent that for many years they were much lower than dividend yields.

The recent movements in fixed income markets has reversed this and investment-grade corporate bond yields are now substantially higher than dividend yields.

Investors are now being meaningfully compensated for taking on high-quality credit risk. This is likely to attract more income-seeking buyers into the asset class.

UK corporate bond yield versus UK equity dividend yield

Source: Bloomberg as at October 28 2022

Source: Bloomberg as at October 28 2022

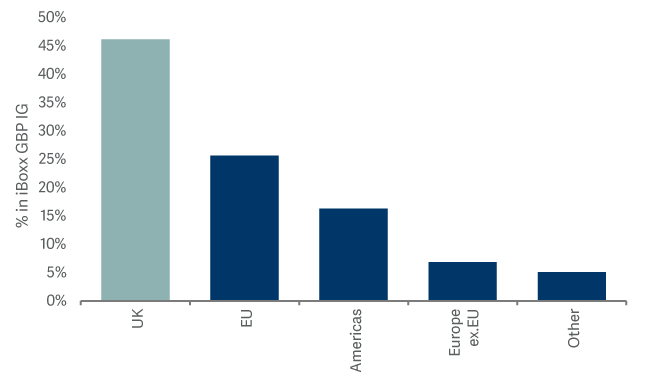

3. GBP credit is not UK credit

The UK suffered a hit to its economic credibility in September because of the actions of the last government.

While the new government has restored confidence, sentiment may remain fragile. This should not really affect investment in the corporate bond market, as, much like the FTSE 100, the majority of its earnings are generated overseas.

45 per cent of the constituents of the investment grade index (iBoxx GBP) are businesses registered in the UK, but only 20 per cent of their revenues are generated in the UK, so it remains a very international market.

GBP credit is not UK credit

iBoxx GBP IG country of risk1

Source: 1Artemis, IHS Markit as at 5 October 2020.

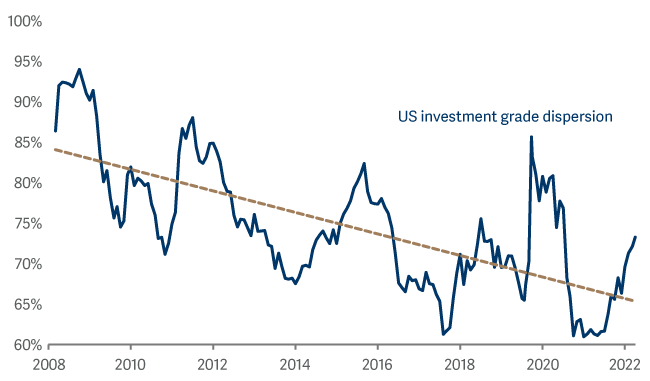

4. Dispersion is increasing in the corporate bond market

During the decade or so of quantitative easing, it was a case of a rising tide lifting all boats: there was always a buyer for corporate bonds in the shape of the central banks.

As QE gives way to quantitative tightening, the situation looks very different. Chart 4 shows dispersion in corporate bond returns since 2008.

100% is the maximum difference between winners and losers, such as during the Global Financial Crisis when bank bonds fell markedly and defensive bonds such as utilities soared.

During the years of QE, the line has been cyclical but has trended downwards. It has recently started to pick up as QE has been withdrawn.

This, and the increase in volatility in the market, creates a very fertile environment for active managers.

Stock selection of increasing importance in a post QE world

Credit market dispersion

Source: BofA Merrill Lynch as at September 30 2022. Note: spreads trade outside +/- 25bps of the index.

Source: BofA Merrill Lynch as at September 30 2022. Note: spreads trade outside +/- 25bps of the index.

Stephen Snowden manages the Artemis Corporate Bond Fund alongside Grace Le

FOR PROFESSIONAL AND/OR QUALIFIED INVESTORS ONLY. NOT FOR USE WITH OR BY PRIVATE INVESTORS. CAPITAL AT RISK. All financial investments involve taking risk which means investors may not get back the amount initially invested.

The Artemis Corporate fund is a sub-fund of Artemis Investment Funds ICVC. For further information, visit www.artemisfunds.com/oeic.

Third parties (including FTSE and Morningstar) whose data may be included in this document do not accept any liability for errors or omissions. For information, visit www.artemisfunds.com/third-party-data.

Any research and analysis in this communication has been obtained by Artemis for its own use. Although this communication is based on sources of information that Artemis believes to be reliable, no guarantee is given as to its accuracy or completeness.

Any forward-looking statements are based on Artemis’ current expectations and projections and are subject to change without notice.

Issued by Artemis Fund Managers Ltd which is authorised and regulated by the Financial Conduct Authority